WINTER IS HERE! It may be midsummer out there, but the chill of an economic slowdown has started setting in deep. Many people in the government had seen it coming, but were asked to keep quiet. The price of the silence has now become a heavy burden on the economy.

Despite the Modi government’s official narrative of India being one of the fastest growing economies in the world, the distress signals are showing up across reports. North Block these days receives calls from almost every multilateral agency and foreign fund expressing concerns about India’s growth trajectory.

Railway Minister Piyush Goyal, who held the finance portfolio for a brief period, said no matter what the talk was, India was one of the fastest growing economies. But Goyal’s claim is taken only with a pinch of salt. “Sure, we are one of the fastest growing economies right now, but that is because there is a slowdown in China,” said Madhur Jha, research head of Standard Chartered Bank in India. “The Indian economy has grown faster than this in the past.”

Jha in a recent report said that India’s per person GDP of about $1,970 would become $5,400 by 2030. However, Bangladesh’s per person GDP ($1,600 now) would touch $5,700 by then and Vietnam’s $10,400. China’s per person GDP of $8,807 will continue to grow at 5 per cent or more till 2030.

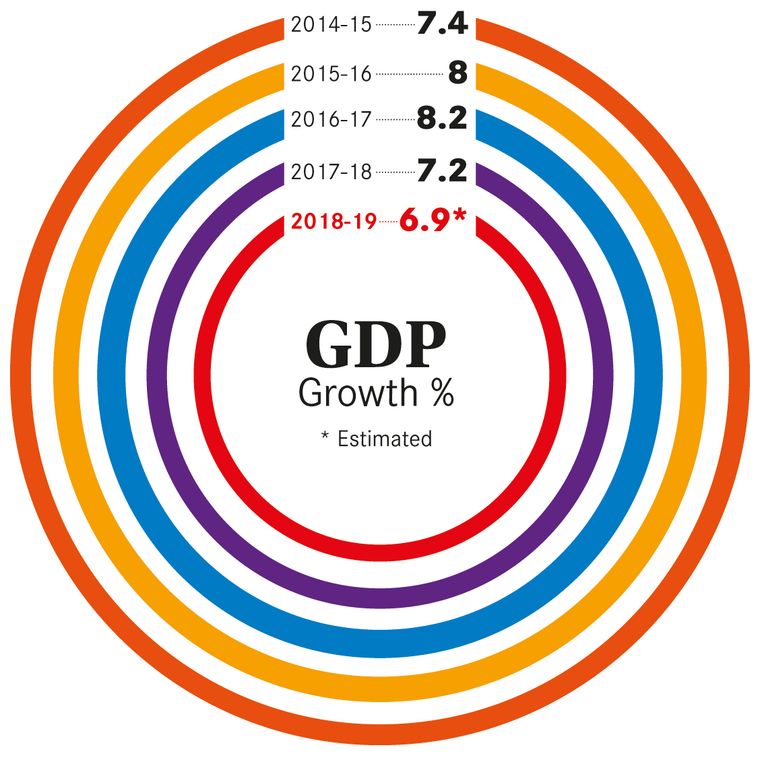

The concerns over India’s growth engines sputtering were triggered by Asian Development Bank, which has big investments in large infrastructure projects in India. The ADB revised India’s GDP estimate downwards to 7.2 per cent in April, from 7.5 per cent earlier. Subsequently, the Reserve Bank of India dropped its expectations on GDP growth hovering above 7.5 per cent for 2019-20. The World Bank and the IMF had also expressed concerns about India’s GDP growth for the year and pegged it at 7.2 per cent and 7.3 per cent, respectively.

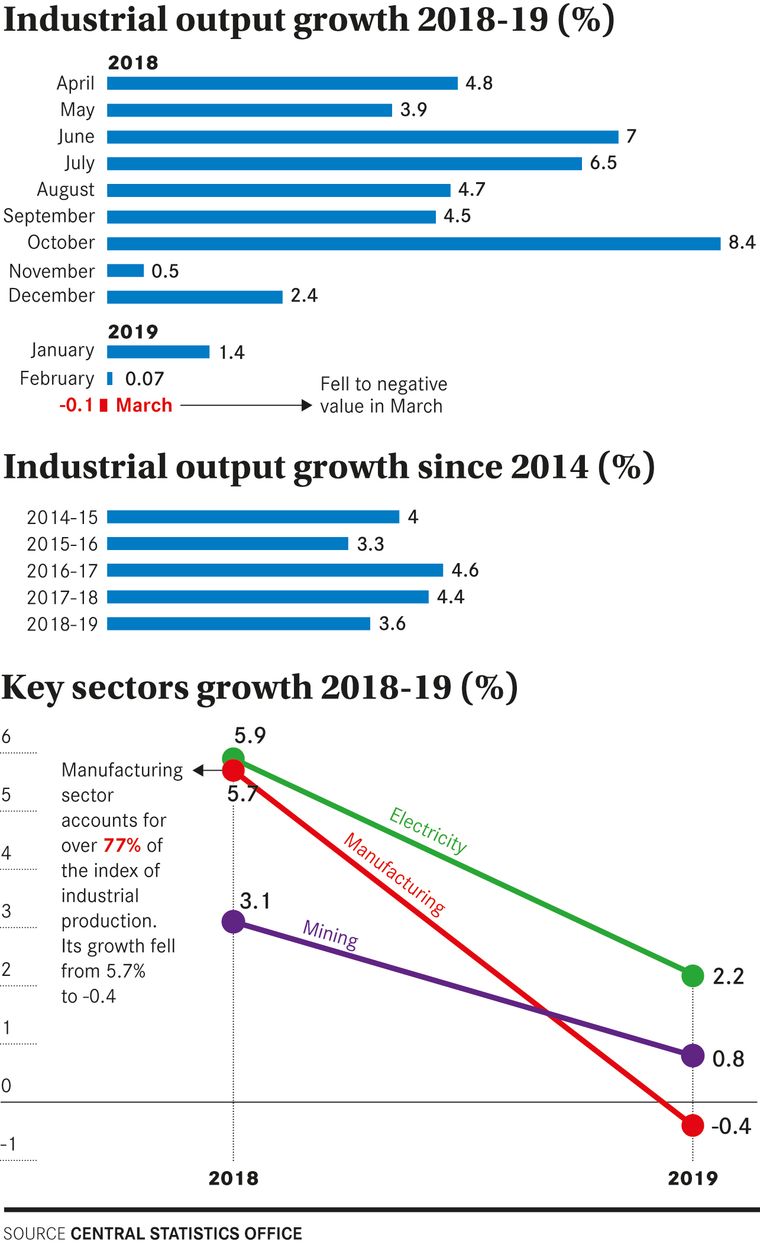

The worry lines started appearing in official estimates of the economy soon, with a monthly economic report of the finance ministry first mentioning fears about a dithering economy with slowing demand. The government numbers tell only half the story. The IMF had warned about high inflation in India, triggered by high fuel prices and some other causes. The finance ministry’s monthly economic report, too, showed consumer and wholesale inflation inching up to 4.2 per cent, higher than 3.8 per cent in 2017-18. “In line with declining real GDP growth, private consumption in Q4 of 2018-19 has also declined,” the finance ministry report said, citing declining sale trends in two-wheeler and automotive sales in the past few months.

“In the month of April, sales dropped by 17.3 per cent across all auto makers,” said Sugato Sen, deputy director general, Society of Indian Automobile Manufacturers. “For many of our members it is like no one is ready to buy at any price point right now.”

The small auto component manufacturers are also having a tough time. “In Manesar and Gurgaon, many small component manufacturers are operating at less than 40 per cent of their capacity,” said A. Venkatramani, president, Automotive Component Manufacturers Association of India. “The bigger auto component manufacturers are also feeling the pinch because of lower domestic auto sales.”

Two years ago, many in the government had identified the early symptoms of what could become an ailment for the entire economy. Nothing showed up in the official reports as they were restricted from airing their concerns over glossing of benefits of demonetisation and the goods and services tax. T.C.A. Anant, former chief statistician of India, however, voiced his concerns. “There is an alarming decline noticed in the rate of household savings,” he warned at the beginning of 2018. “This implies that incomes have fallen and people have less disposable earnings in hand. It will translate to lower appetite for bank credit going ahead.”

His fears are now being reverberated by other economists. “Exports have dropped in the last five years. This was triggered by an appreciating effective exchange rate. The currency volatility makes it more difficult for exporters to fix a deal. This drop in exports was exacerbated by a slowdown of the manufacturing sector. This dealt the final blow,” said trade economist Rupa Chanda, professor of economics at IIM-Bangalore, who officiates as a member of the standing committee on services at the Central Statistics Office, indicating that closure of many small manufacturing units post demonetisation and GST has impacted India’s export volumes. She said exporters across India suffered because of the hostile trade environment in many countries and lack of enough incentives.

A case in point is leather goods exports, which form a considerable portion of India’s export basket. The sector, once thriving with orders from the European Union and southeast Asia, has witnessed a sharp slump in business. “Uttar Pradesh produces about 31 per cent of all our export orders. This year, with the kumbh mela event, many tanneries in Kanpur region were asked to close down months ahead,” said Aadhar Sahni, president, Indian Leather Products Association. “Even three months after the kumbh mela, more than 1,000 units in Kanpur region are still awaiting the state government’s permission to start operations.”

A bigger problem is in the agricultural sector. “There are unmistakable signs of India’s economy slowing down over the last few years,” said Kaushik Basu, former chief economic adviser and professor at Cornell University, at a lecture in IIM-Ahmedabad. “A majority of this has been caused by the slump in the agriculture sector’s contribution to GDP in the past few years.”

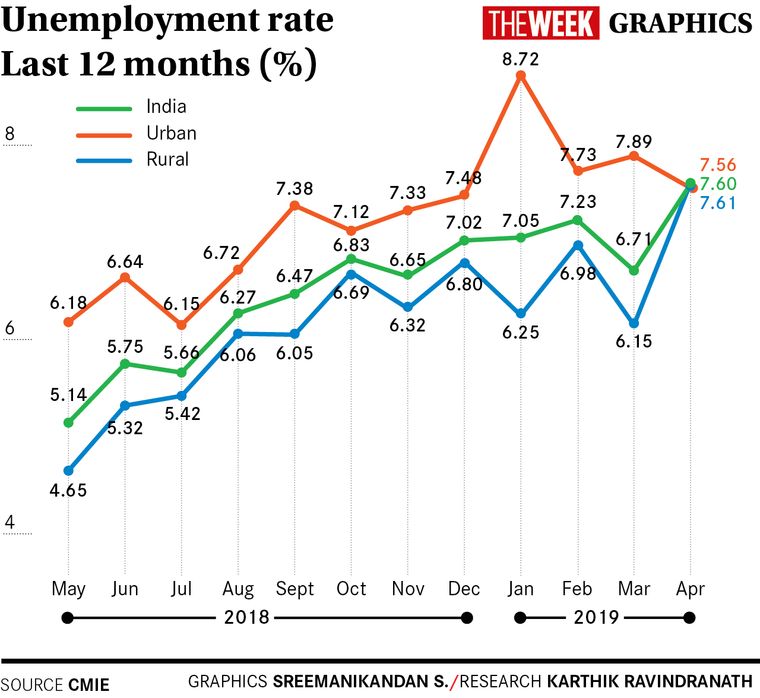

Then there is the concern over unemployment. Basu said the jobs situation was most worrying. “If you put together all the piecemeal data coming in, it is clear that our workers are suffering greatly, with unemployment rate at over 7 per cent, according to the Centre for Monitoring the Indian Economy, and youth unemployment at 16 per cent, as per a study by Azim Premji University,” he said. He called for a re-look at inculcating professionalism in policymaking based on ‘data’ and ‘reasoning’ and curbing disproportionate focus on large businesses to reverse the economic slowdown.

Basu’s views found resonance in that of another eminent economist, Rathin Roy, chairman of the Prime Minister’s Economic Advisory Council. “So far, growth has been spurred by catering to the demands of the top hundred million, which is why indicators of economic performance are about sales of cars, two-wheelers, air conditioners and upmarket housing. The goods that are consumed by all 1.2 billion Indians—nutritious food, affordable clothing, affordable housing and affordable health and education—do not figure.”

Roy told THE WEEK that the rural distress was at the heart of the current economic slowdown. “If the share of these goods in the composition of GDP growth does not increase, we will be in a middle income trap,” he said. The middle income trap is a theoretical situation in which a country that attains a certain income gets stuck in that level. Roy said he had not spoken out to undermine the government but to give a realistic picture of the economy to political parties before the parliament elections. “In my view, reform of government economic administration must take priority,” he said. “As things stand, it is a prerequisite for the success of any other reform. A weak state cannot deliver anything other than grandiloquent statements of intention. This must change. Without a capable state, there can be no transformation.”

A few days after Roy spoke out, serious flaws in economic policymaking were uncovered by a technical report of the services sector, which was prepared as part of the 74th survey round of the National Sample Survey Office. The report indicated the possibility of the government overestimating the GDP contribution of the private sector. “What came up during the technical study of the services sector numbers was that the MCA-21 corporate database (an e-governance project of the ministry of corporate affairs) could have some reliability issues,” said Jyotirmoy Poddar, director general of NSSO, a day after the paper was released.

Since the release of the controversial paper, Poddar, who holds the post of chief statistician of India and secretary in the ministry of statistics and programme implementation, has been on leave. The finance ministry, however, defended the anomaly, saying that the overestimation as indicated by the body was only to a little extent in the estimation of the overall GDP, and not for the year-on-year GDP growth percentage.

“These 36,454 companies indicated by the NSSO as out-of-survey companies are also part of the overall GDP of the country,” said Finance Minister Arun Jaitley. However, the government moved the report for a detailed study by a standing committee on services under the ministry of statistics and programme implementation and chief statistician.

Earlier, the National Statistical Commission, the government’s apex independent economic data policy body, had witnessed a spate of resignations over the allegations of the government suppressing the jobs data for more than two years. Currently, the commission is virtually defunct as five positions in it are vacant.

“It is high time that the government laid more emphasis on data collection and had the courage to reveal and act on these data,” said N.R. Bhanumurthy, professor at the National Institute of Public Finance and Policy. “A need of the hour is probably investing more in systems and manpower at our age-old economic data collection bodies. Most of these today are burdened with tracking the economy that has grown by leaps and bounds in the past 10 years.”

Experts say the only way to battle the many reasons behind the economic slowdown is an honest reading of economic data. “The rise in GDP based on performance of companies on the MCA database was never a reliable methodology,” said R. Nagraj, professor at Indira Gandhi Institute of Developmental Research and a supporter of the earlier system of calculating manufacturing data through the Annual Survey of Industries. “The government would do great service to everyone, if only it resorts to a more realistic computation of the GDP.”

As the nation awaits a new government, economists say its challenge would be bringing the economy back on track. “In all likelihood, growth would not improve immediately after a new government at the centre takes charge,” said Madan Sabnavis, chief economist at CARE Ratings. “Going ahead, all eyes would have to be on employment generation, or else the consumption-driven growth story of India could be just another mirage.”

Expert’s view

D.K. Joshi, chief economist, CRISIL

D.K. Joshi, chief economist, CRISIL

What is slowing down the economy?

Domestic factors are largely responsible. There has been a slowdown in agriculture growth. Farm income and wage growth have been weak. It hurts consumption demand. Exporters also faced glitches. Then there is the NBFC-related credit crunch. The government’s ability to support the economy through the budget is also reducing, because it is running high fiscal deficits.

How long would it last?

It will depend on what kind of monsoon you get and what happens to oil prices. If they are favourable, you will see a lift. Otherwise, the headwinds will be much more and that will require the government to step in.

What should the government do?

GST and bankruptcy code are works in progress and need to be streamlined. Petroleum products should be gradually brought into GST. On the bankruptcy code, we are seeing improvement in the number of cases being sorted out, but the time it is taking is still quite long. Reforms that will improve the operational efficiency of public sector banks are needed. There has to be a policy to address the agriculture economy. Should revive private investment.

—NACHIKET KELKAR

Expert’s view

Mohan Guruswamy, economist and chairman Centre for Policy Alternatives

Mohan Guruswamy, economist and chairman Centre for Policy Alternatives

What is slowing down the economy?

India’s economy is government expenditure driven. Capital expenditure generates employment and creates a large multiplier effect. In the last two years, capital expenditure has dropped. Capex is related to your savings to GDP ratio. Savings to GDP ratio gives you tax to GDP ratio. When you have a good tax to GDP ratio, you will get good expenditure to GDP ratio. All the ratios have been coming down. For 13 consecutive quarters, savings ratio has come down. So, you are not buying vehicles or even fast-moving consumer goods. When consumption drops, production drops, and when production drops, job creation drops.

How long would it last?

The trend had begun in the last two years of the Manmohan Singh government. Unemployment rate has been highest in 45 years. India is losing a chance of getting out of the middle-income trap. You will just limp along. There are many countries like that. We may end up like those.

What should the government do?

Stimulate demand. You have to make agri produce more remunerative. You need to create more jobs. Construction industry must expand to create low-skill jobs. You need to create at least three million low-skill jobs a year. The new government will have to look at the key ratios and review them every month. Savings to GDP ratio must be over 40 per cent. If you increase taxation, you will be able to spend more money.

—NACHIKET KELKAR

Expert’s view

Madhavi Arora, economist, Edelweiss Securities

Madhavi Arora, economist, Edelweiss Securities

What is slowing down the economy?

Limited consumption stimulus by the government amid fiscal constraints. The investment appetite has also faded ahead of election uncertainty. Private capital expenditure is sluggish. Rural demand has weakened and is unlikely to be reversed soon amid structural issues in the farm sector and the vagaries of monsoon.

How long would it last?

Marginal cyclical improvement in growth is expected in FY20 amid easier monetary stance and some consumption-led fiscal push. Domestic structural overhang and global slowdown concerns are constraining significant pick-up in growth. May see some pick-up in investment appetite in a stable political regime.

What should the government do?

Policy focus should be on structural measures rather than mere policy rate cuts or looser fiscal stance. Need to work on structural, land, labour and financial sector reforms to improve the productivity of the manufacturing sector and boost growth. The manufacturing sector requires exports impetus.

—NACHIKET KELKAR