They came from far and wide to Mumbai, filling up the vast Cooperage Football Ground in Colaba, excited like a teenage ARMY at a BTS concert. It was not a match or a concert, though; yet the man who made them go there was a rock star on his own.

It was the mid-1980s and Dhirubhai Ambani had kickstarted a stock market revolution with the initial public offering of Reliance a few years earlier, turning thousands of ordinary Indians across the country into crorepatis. And in the ‘go-big-or-go-home’ style that has encapsulated the Ambani business ethos, the annual general body meeting of the company was held in a stadium, a first, perhaps, in the world.

“I knew history was being made,” said Ramnikbhai, an early Reliance investor whose life was transformed because of that one nifty bit of investment. Rs1,000 invested in the Reliance IPO is worth more than Rs2 crore today!

Will history repeat itself and cash counters go cha-ching again, as the Life Insurance Corporation of India, India’s largest insurer, gears up for its first sale of shares? Will it, in the process, help the government avoid a debt trap? More significantly, will it change the way Indians invest, making ordinary people put their money in stock markets for the first time?

TAKING STOCK

V.R. Srinivasan, a bureaucrat based in Delhi, had stuck to safe modes of investments like fixed deposits and insurance policies all his life. The ‘riskiest’ he had ever gone was putting a small amount in a systematic investment plan. Now, just a few months ahead of his retirement, all that might change.

Changing lives, everywhere: An LIC office in Kolkata. One in every four Indians has an LIC policy | Salil Bera

Changing lives, everywhere: An LIC office in Kolkata. One in every four Indians has an LIC policy | Salil Bera

“Markets are unpredictable, but there is definitely value in LIC IPO,” he said. “I will apply for a minimum number of shares.”

On offer are 22.14 crore shares that could mop up around Rs21,000 crore, which would make it the biggest ever IPO in India. The government is diluting just 3.5 per cent of its stake. Even in a season of big bucks and big listings, it is huge. “LIC is the elephant that has entered the room; it is a signal to the whole world,” said Sethurathnam Ravi, former chairman of the Bombay Stock Exchange. “By width and depth, LIC is like the Indian Post Office—it’s in every corner. What it will do is that many conservative people who have not come into the stock market so far will start investing through this. That is going to be a game-changer.”

Hoping for the best: Mahendra Pal Singh, a security guard in Delhi, is keen on buying LIC shares | Sanjay Ahlawat

Hoping for the best: Mahendra Pal Singh, a security guard in Delhi, is keen on buying LIC shares | Sanjay Ahlawat

LIC, clearly, is no ordinary company going to the stock markets to raise some money. Formed by an act of Parliament by merging 245 private insurance companies in 1956, it is the fifth-largest insurer in the world in terms of gross premium. The company has more than one lakh employees, nearly 5,000 offices and about 14 lakh agents. It manages assets worth Rs38 lakh crore, which is a whopping 15 times more than those managed by SBI Life, the second biggest insurance company in India. “Listing of LIC is a phenomenally positive move,” said former finance secretary Subhash Chandra Garg. “I have been arguing for this for the past four years. It is the right way to go.”

Size matters: An LIC office in Delhi. LIC is the fifth-largest insurer in the world in terms of gross premium | Bhanu Praksh Chandra

Size matters: An LIC office in Delhi. LIC is the fifth-largest insurer in the world in terms of gross premium | Bhanu Praksh Chandra

The company has about 29 crore policyholders. That is, one in every four Indians holds an LIC policy! And they will be key to the success of its mammoth IPO, as the regular stock traders, the ‘big bulls’ and institutional investors, may not be enough for a stock sale of this size.

Sethurathnam Ravi

Sethurathnam Ravi

The government wants the policyholders to chip in by buying into their insurer and has set aside 10 per cent of the total equity shares on offer exclusively for policyholders and employees, at a discount. LIC had gone on an overdrive of advertisements and public campaigns, calling on policyholders to update their PAN number and become eligible to apply for this 10 per cent, and pushing LIC agents to get the message across.

That could help people like Mahendra Pal Singh. His job as a security guard at an apartment complex in Mayur Vihar in Delhi feels like a world away from that of the bulls and bears of Dalal Street. But that is about to change.

“I earn very little, which is entirely spent on household expenses and children’s studies,” said the 49-year-old from Mathura in Uttar Pradesh. “Normally I don’t get to save much—I have taken a couple of LIC policies; those are my only investments.”

But his interest has been piqued by his friendly neighbourhood LIC agent who told him about the upcoming IPO and that he was eligible to apply. “LIC is a sarkari brand, a big name,” he said. “I would like to apply for the shares.”

Everyone, like Singh, counts. 2021 was a bumper year in which IPOs raised Rs1.2 lakh crore in India; in 2019, it was just above Rs12,000 crore and in 2020, about Rs26,000 crore. “The size of this IPO is large not only in absolute numbers but large in relation to how much IPO the Indian market can absorb in a year,” said Apoorva Javadekar, professor of finance at the Indian School of Business, Hyderabad.

DOUBLE ENGINE STRATEGY

The fear of all shares not getting snapped up is giving mandarins in North Block and CGO Complex sleepless nights. Foreign portfolio investors have pulled out more than Rs1.26 lakh crore from Indian equity markets in 2022. This is in addition to the Rs38,500 crore they pulled out between October and December 2021. On April 26, the Sensex was down 1.5 per cent from January 1, and around 8 per cent from October 19, 2021, its lifetime high. Also, some of the insurance companies have felt the selling pressure. ICICI Prudential Life Insurance and HDFC Life, for instance, have tumbled more than 25 per cent from their 52-week high. SBI Life went down 15 per cent from its peak.

Even if you take just the 10 per cent kept aside for LIC policyholders, the LIC IPO would require crores of applications from retail investors (meaning ordinary citizens) to succeed. The biggest public participation seen so far in India was 48 lakh applications received for the Reliance Power IPO in January 2008. Depending just on the regular stock traders might not be enough to pull that off. LIC’s strategy? Ride on the ‘double engine’ of crores of its ‘older’ policyholders who may never have bought shares until now, as well as entice the app-happy new-gen who have taken to share trading since the advent of the pandemic.

For the stock market-ignorant policy holding crowd, LIC has been on a media blitzkrieg, giving full-page ads and setting up shamianas in a nationwide exercise. For instance, Axis Securities alone opened 1,000 counters outside LIC offices across the country to meet and advise policyholders on how to open demat accounts. (A ‘dematerialised account’ holds shares and securities in an electronic format, and it is needed for buying shares.)

The company also sent out a clarion call to its unique asset—14 lakh agents all over the country. “We have been told to spread the word around and help customers get their demat accounts set up and figure out how they can apply for the IPO,” said Vijayalakshmi R. Ratnam, an LIC agent in Delhi.

For the younger crowd, finfluencers, bloggers and video creators have been roped in to run digital campaigns on social media. Religare Broking, for instance, launched the Pre-Apply LIC IPO app. “To this young generation, LIC may not appeal as a risk partner. But when it comes to investing, it definitely will,” said Ajit Misra, vice-president & senior technical analyst with Religare Broking.

Harshad Patel, 29, said he would bite. He runs a plywood business in Delhi and has been dabbling in stocks for a few years. “I am interested in the LIC IPO, and I invest for the long term,” he said. “There is a lot of interest in this among friends in all my WhatsApp groups.”

Jagadeesh, a corporate executive at an Indian multinational in Chennai, has been trading shares ever since he started working. He, however, might not pick up the LIC scrip because he did not see it as a great opportunity, but admits that it is making a lot of noise. “It is certainly creating the kind of craze that Ambani sparked off in the 1980s,” he said. “A lot of boom, for sure!”

LOCK, STOCK AND BARREL

It is a boom that India needs. The economy was already locked down in a slowdown rut when the idea of an LIC stake sale was first mooted in the 2020 budget, but things only got worse from then on with the national lockdown and continuing pandemic pains.

Through budgets and stimulus packages, Finance Minister Nirmala Sitharaman has been betting big on spending big to get India out of Covid’s impact. But it comes at a cost—the total liabilities hit an all-time high of 90 per cent of the GDP during the pandemic, according to the International Monetary Fund. It is the highest among emerging countries. A third of this debt was added in the past three years.

There are rules capping fiscal deficit (the difference between the money the government makes and the money it spends) at 3 per cent, but this has been thrown to the wind in the past two years in the name of Covid. In 2021, India’s fiscal deficit was 9.2 per cent. The deficit is slated to remain above 6 per cent at least for another two or three years.

Of course, a government can borrow infinitely, but it comes at a cost. “Right now, we have maxed out,” said Javadekar. “There are huge repercussions if we borrow more. India is already sitting at the lowest of investment-grade ratings. Further borrowing, coupled with not meeting disinvestment and fiscal deficit targets, could mean rating agencies lowering India to non-investment grade.” That means foreign investors leaving the country and a diminished borrowing ability of the government.

More woes abound. The National Monetisation Pipeline, a grandiose plan to earn Rs6 lakh crore by leasing out public assets to the private sector, has come a cropper because of the stringent conditions and low interest. Sitharaman, in her budget on February 1, cut the divestment target for 2021-22 sharply to Rs78,000 crore from Rs1.75 lakh crore. Eventually, with the LIC IPO getting postponed, the actual divestment receipts were only Rs13,531 crore. In the current financial year, the government is expecting a modest Rs65,000 crore from stake sale in state-owned firms.

Oil prices soaring due to the war in Ukraine means not just a spike in import bills, but also a rise in the prices of almost everything. Inflation is inching up to a point it will hurt. The oil spike has also meant that many of the government’s calculations for bettering its financial health have gone for a toss. Many budget plan projections were drawn up based on an average oil price of $75 to $80 a barrel—though at $89 on the day of the budget, it shot up to $127 in a month, catalysed by the conflict in Ukraine.

This makes it imperative for the government that the LIC IPO sails through, mopping up not just the desperately needed revenue for budget schemes, but also enough to meet targets that determine India’s future ratings. But, has the government’s wait for a perfect timing for the IPO instead led it to a perfect storm that can upset the best-laid plans?

SEXY OR SENSELESS?

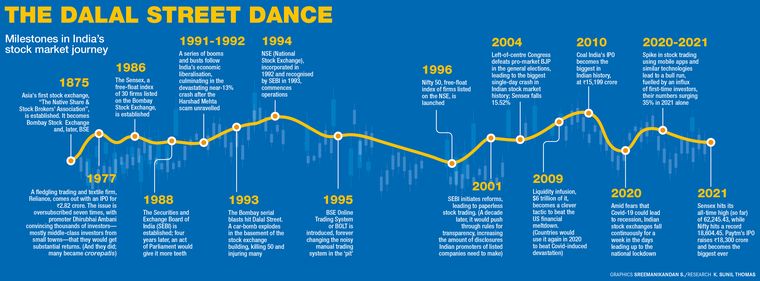

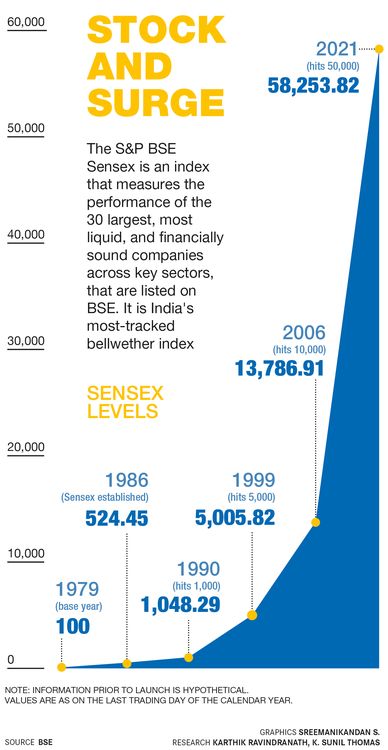

Vikram Samvat year 2077 which ended with Diwali last November was a period of unprecedented bull run, despite the deadly second wave of Covid and the pandemic-induced economic pains. The Sensex, the BSE index, went up an astonishing 40 per cent in value during this period, with investments by the likes of ‘big bull’ Rakesh Jhunjhunwala growing 150 per cent since Covid hit.

“You could even say the Sensex took leave of its senses,” said author T.N. Ninan in a column. The reasons are not difficult to see. After Covid’s impact, governments around the world reduced interest rates and injected oodles of cash into the system in an attempt to stimulate economic activity. This easy money made its way into the capital markets everywhere, especially into India, on which foreign investors bet big.

Parallel to this was the trend of first-time investors in India turning to stock markets, owing to the falling fixed deposit rates, and the realisation that assets like property do not serve the sudden need for money when crises like Covid hit.

Just about four lakh new demat accounts were created in 2019; it tripled to 12 lakh after Covid hit. Spurred by this rush of ordinary citizens to invest their money in stocks, Indian companies, especially those in the tech space whose original investors wanted to cash out, rushed to the bourses. While 16 IPOs came to the markets in 2019, the number shot up to 63 last year. This included the likes of Zomato, which mopped up nearly Rs10,000 crore, and Paytm, which raised Rs18,300 crore.

The Air India privatisation finally going through seems to have spurred the government to shift into top gear with the LIC IPO, and the stars of the new Samvat suddenly have turned their lights on Sitharaman & Co. Through the initial months of 2022, the Sensex has been on a wild see-saw, wiping out thousands of crores of investor money.

Even while the government went through the steps—rules were changed to let foreign investors buy LIC shares and the red herring prospectus got approval by SEBI, the market scenario only turned from bad to worse. If the US Federal Reserve’s move to tighten liquidity and the rise of new Covid variants were not enough, the Russia-Ukraine conflict and subsequent oil price spike saw the markets going steadily into uncertain territory.

HEALTHY, WEALTHY AND WISE

A successful listing outweighs the potential risks. And ‘right-sizing’ the issue was a good move. The valuation was “fair and attractive”, said Tuhin Kanta Pandey, secretary, Department of Investment and Public Asset Management. “We want to champion LIC as a long-term value creator in the equity markets. The IPO is the first step of long-term value creation for LIC shareholders.”

“The pricing is pretty attractive,” said Avinash Gorakshakar, director (research) at Profitmart Securities. “Perhaps the government wants to offer a little better carrot, which will go positively. Several fund managers have indicated that valuations are decent.”

In return, the government will not only get to improve its fiscal health and fund infra projects but also get a solid stamp of approval for its pro-reform credentials. But the biggest impact could be in how it will change what Indians do with their money. Said a Mumbai-based financial expert with a leading consultancy who did not want to be named because the firm has a policy against speaking about individual companies, “The entire ecosystem is falling into place. People are getting wiser regarding their investment choices and risk-taking ability.” The LIC IPO could be just what they need to take the plunge.

WITH NACHIKET KELKAR