Dharmakirti Joshi

Dharmakirti Joshi

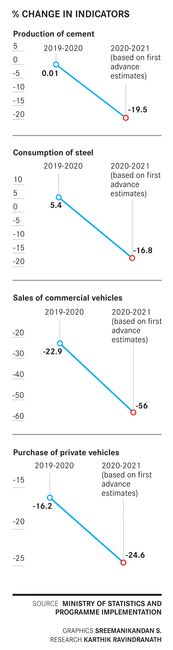

Finance Minister Nirmala Sitharaman has promised a budget like “never before”. Hyperboles apart, the economy, ravaged by the pandemic, needs an extraordinary effort from her part to get back to any semblance of normalcy. The gross domestic product contracted a record 23.9 per cent in the April-June quarter and the unemployment rate in December was at a six-month-high of 9.1 per cent. The expectation is that the government will go big on spending in infrastructure and other critical sectors, while also injecting a stimulus to the worst-hit sectors.

The crucial question, however, is, where is the money?

The Centre’s fiscal deficit (the difference between its income and expenditure) was Rs10.75 lakh crore at the end of November 2020, which is 135 per cent of the estimate for 2020-21. Till November end, the government’s total receipts stood at Rs8.31 lakh crore, which is just 37 per cent of the estimates for the financial year ending on March 31. The tax collection revenue was just 42.1 per cent of the estimates.

In the last budget, the government had set a lofty target of raising Rs2.1 lakh crore by selling stakes in public sector enterprises. A large chunk of it was expected to come from stake sales in the Life Insurance Corporation of India, IDBI Bank, Air India and Bharat Petroleum (BPCL). However, it has managed to raise only Rs13,844 crore. While the process of LIC going public is under way and expressions of interest have been invited for Air India’s sale, they are unlikely to happen by March.

The Indian economy had slowed down even before the pandemic hit, which had constrained the government’s ability to provide a huge stimulus. But it announced measures worth Rs30 lakh crore in the last nine months. A large part of it, however, was on credit guarantees and measures like giving option to government employees to encash their leave travel allowance for the year. With the GDP expected to contract 7-8 per cent this year, clearly there is a need to do much more.

Arun Singh

Arun Singh

“The scope for revenue will be better in 2021-22 as the economy will rebound and tax collections will pick up,” said Dharmakirti Joshi, chief economist at the ratings agency CRISIL. “Still the scope for a very strong stimulus is not there. So, you have to do more with less. It essentially means, focus on areas that require the most attention and where you get the maximum multiplier effect for the economy.”

In the current fiscal, duties on petrol and diesel were raised by Rs10 and Rs13 a litre, respectively. An increase of one rupee in excise duty on auto fuels results in an additional revenue of Rs12,000 crore a year for the government. The share of excise duties in gross revenue is likely to rise to 18 per cent in 2020-21, from 12 per cent in 2019-20.

According to M. Govinda Rao, member of the fourteenth finance commission, the improved Goods and Services Tax collection (a record Rs1.15 lakh crore in December and more than Rs1 lakh crore in every month since October) do offer some hope about revenue. Yet, he said, the tax revenue collection would remain subdued in the current financial year and a substantial part of the next year. “Unfortunately, the government does not have enough resources to pump prime the economy by increasing public spending. Next year will present greater opportunities to fast-track strategic disinvestment not merely to raise resources for revival, but also to vacate the government’s involvement in non-strategic areas,” he said.

Even as the government pushes for privatisation, experts call for a focused approach on increasing foreign investment limits in various sectors. The production-linked incentive scheme recently announced by the government has seen a lot of takers. “India has a cost advantage,” said Arun Singh, global chief economist at Dun and Bradstreet. “Government support is there, labour support is there, cost efficiency is there and global companies are able to get a big domestic consumption market for their goods. So, a well-calibrated plan is required, which will be a big opportunity to push the Make in India initiative. You can increase the FDI cap to get additional funds.”

Investment as a percentage of the GDP is expected to fall sharply in the current financial year, and experts say the private sector needs to be encouraged to invest more. “The government needs to revive investment, particularly in infrastructure, because infra investment is largely supported by the government and private sector generally is not enthusiastic in participating in it,” said Joshi. He said this could be changed by reforms that would help private players raise funds easier and balance the risk of long gestation periods in the infra sector.

The government had increased the borrowing target to Rs12 lakh crore this year, and had raised Rs9.05 lakh crore till December. Globally, interest rates are at record lows, as governments and central banks pumped in billions of dollars in fiscal and monetary stimuli. It is an opportunity for India. “They can raise funds at lower costs given excess liquidity in many of the markets, and interest rates are also low. At the same time, it will leave room for the states and private enterprises to borrow funds from the local market,” said Singh.

The Fiscal Responsibility and Budget Management (FRBM) Act mandates that revenue deficit, fiscal deficit, tax revenue and the total outstanding liabilities must be projected as a percentage of the GDP in the medium-term policy statement. The set targets could be exceeded only in case of a calamity or national security issue. In the current financial year, the wider expectation is that the fiscal deficit will be significantly higher than the 3.8 per cent in the previous fiscal. Rao expects it to be in the 7.5-8 per cent range in the year ending March 2021, against the budget estimate of 3.5 per cent.

With the budget expected to focus on stimulus and boosting investment, fiscal consolidation is likely to take a back seat. “You need to keep the FRBM on the side right now,” said Joshi. “But at the same time, give a medium-term direction on how you intend to correct the fiscal imbalance. That need not be done in 2021-22, because you do need to spend more.”