Dhanji Street in south Mumbai’s Zaveri Bazaar is dotted with jewellery stores and diamond merchants. It was here that the young Gautam Shantilal Adani got his first taste of trading in the 1980s. He sorted stones at a diamond merchant’s place in the mornings, and then went to college. Soon he became so good at the job that he dropped out to become a full-time diamond trader.

Diamond trading requires quick thinking and swift action. You buy diamonds in one country, trade them in another, cut them in yet another one and then sell the finished stones in a totally different country. This experience has perhaps helped Adani to build an empire that now spans coal mining and power generation to running ports and airports.

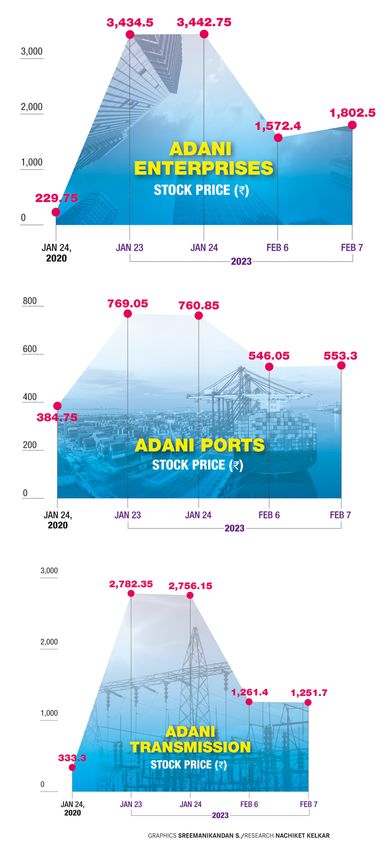

As his business expanded, the stocks of his companies became the darling of the market. The group’s flagship, Adani Enterprises, for instance, surged from Rs229.75 on January 24, 2020 to Rs3,434.50 on January 23, 2023―a 1,384 per cent increase. Some of the other group stocks like Adani Ports, Adani Power, Adani Transmission, Adani Green Energy and Adani Total Gas gained between 99 per cent to as much as 2,120 per cent in this period.

Their fall from the peaks was equally spectacular, after a report by US-based short-seller Hindenburg Research sent shockwaves across the markets on January 24. The report accused Adani Group of engaging in “brazen stock manipulation and accounting fraud scheme over the course of decades”, and also pointed to the “substantial debt”, including pledging shares of the inflated stock for loans, putting the entire group on precarious financial footing.

The stinging report came just a few days before the opening of Adani Enterprises’ follow-on share sale to raise Rs20,000 crore, prompting the group to quickly react. “The report is a malicious combination of selective misinformation and stale, baseless and discredited allegations that have been tested and rejected by India’s highest courts,” shot back Jugeshinder ‘Robbie’ Singh, group CFO, a day after the Hindenburg report was released. A few days later, Adani Group released a 413-page response to Hindenburg’s allegations.

Despite the spirited defence, the shares of eight listed Adani companies were under intense selling pressure since the report released. Between January 24 and February 6, Adani Enterprises shares corrected 54 per cent and Adani Total Gas slumped 60 per cent. Other group stocks fell between 28 per cent and 54 per cent. Even, the cement makers Ambuja and ACC, which Adani acquired in 2022, declined 24 per cent and 15 per cent, respectively.

Though the Adani Enterprises FPO got fully subscribed―despite retail individual investors staying away from it―owing to strong interest from non-institutional investors, Adani Group withdrew the issue and refunded all investors.

Gautam Adani said the withdrawal was to “insulate the investors from potential losses”. That might not be the only reason, as Adani Group had hoped to widen its shareholder base through the FPO. That plan did not work out, as retail investors gave it a skip. “There might have also been second thoughts over stock prices crashing further,” said a senior executive at a stock broking firm. “Historically, some companies that went public and saw their prices crash later have had to take measures like bonus issue to pacify investors. Instead of all that, Adani might have thought it would be prudent to just return the money.”

Gautam Adani’s first venture was Adani Exports, a commodity trading firm he set up in 1988. Soon he realised that owning a port could provide a base for scaling up the trading business. So, he bought land from the Gujarat government and set up Mundra Port, which became operational in 1998.

Today, Adani Group owns and operates more than a dozen ports across India’s east and west coasts, with an operating capacity of 538 million metric tonnes. It is the largest ports operator in India, handling around 31 per cent of the country’s total cargo volumes.

Adani had the Midas touch. He expanded from trade and ports to power generation, FMCG and construction. He is planning to commission refineries, petrochemicals complexes, specialty chemicals units and hydrogen plants in a petrochemical cluster in Mundra. Adani Airport Holdings is the the largest private airports operator in India, with seven airports in its kitty.

This expansion at break-neck speed has come on the back of several acquisitions and partnerships. The group has also borrowed heavily over the years; to the extent that some analysts say it is over-leveraged. The group, however, denies that. Its net debt to EBITDA (earnings before interest, taxes, depreciation and amortization), which was at 7.6 times in 2013-14, is now 3.2 times, said Jugeshinder Singh. The group has a healthy cash-flow as well.

After the Hindenburg report and the battered reputation, however, the group will not be able to do business the way it used to. “Adani’s bargaining power with banks and external institutions will obviously get impacted. In the existing projects, where the execution is good, that is fine. But, if there is any delay in any project, markets will react negatively,” said a stock broking firm executive.

The Adani companies are already under increased scrutiny. S&P Global Ratings has downgraded its outlook on two group companies to negative. Credit rating agency ICRA said in a statement that the group’s large, debt-funded capital spending programme remained a key challenge.

Financial institutions like Credit Suisse, Citigroup and Standard Chartered have already stopped accepting bonds of Adani Group firms as collateral on margin loans, according to reports. “Sustained selling could trigger debt collateral margin calls on the promoter pledge shares, and this could mean further selling of shares,” said Shriram Subramanian, founder and managing director of the proxy advisory firm InGovern. “Also, the withdrawal of the Rs20,000 crore FPO means that some projects would likely have to be slowed and put in cold storage.”

It is to mitigate this danger that the promoters prepaid around $1.1 billion of debt backed by shares of Adani Ports, Adani Green and Adani Transmission ahead of their maturity in September 2024. Adani Group’s bonds and shares rallied after this announcement on February 7.

The group currently has total debt of about $24 billion. About two-thirds of it is from overseas sources such as bonds or foreign banks and raised using its infrastructure assets or shares as collateral. The dip in the value of its stocks means a corresponding dip in the value of this collateral. This has made lenders cautious; loans will no longer be cheap or easy to come by.

And the group is unlikely to approach the stock market anytime soon. “They will have to tell the market very clearly that nothing was wrong. Till then, probably, they will not come to the market,” said J.N. Gupta, former executive director of Securities and Exchange Board of India and founder of Stakeholder Empowerment Services, a proxy advisory and corporate governance firm. “An independent verification of things will assuage the feeling and restore their reputation. They should engage reputed agencies to everything, a peer audit should be done, so that financial figures are reassured and governance practices are reassured.”

The sell-off in Adani shares has caught the attention of the regulators. SEBI, the markets watchdog, is monitoring the crash and stock exchanges have put several Adani stocks under their additional surveillance measure framework on a short-term basis. Intraday trading in these stocks would require 100 per cent upfront margin, which would curb speculation and short-selling.

The Reserve Bank has sought data from banks on their exposure to Adani companies. Of the group’s total debt, Indian banks account for less than 40 per cent. Dinesh Kumar Khara, chairman of State Bank of India, clarified that loans to Adani Group have been given for projects with tangible assets and adequate cash flows. SBI’s outstanding exposure to Adani Group is about Rs27,000 crore, or about 0.88 per cent, of its total loan book.

After withdrawing the FPO, Adani told investors that his group’s balance sheet was healthy and it would continue to focus on long-term value creation and growth would be managed by internal accruals. They would also continue to focus on timely execution and delivery of projects, he added.

Adani, however, might have to delay new projects and monetise some assets to get out of the woods. One positive thing is many of its projects like ports, airports and cements are well capitalised and have healthy cash flows, and are mostly unaffected by the movement in stock market.

“I find the structure of Adani Group very clean, because there is no cross-holding,” said Gupta. “Every company is standalone and there is no company relationship in the form of investments, loans and advances, except Adani Enterprises, which is like a venture capital company.”

Adani’s biggest assets were his business acumen and political clout. The controversy is likely to diminish his companies’ ability to get lucrative government contracts, which, in turn, will affect the group’s revenue streams. “In the immediate term, the group has to reassure investors that basic company operations are unaffected and all projects are going as per schedule,” said Subramanian of InGovern. “In the medium term, it needs to engage more with the investor community by getting more equity research coverage and also diversify its investor base.”

Many of the group’s new businesses that need huge capital expenditure come under Adani Enterprises. Though the parent company has enough cash to support them, that might not be an ideal arrangement in the long term. Adani Gas and Adani Green have huge debt but limited cash flows, which could become a problem.

The quick-thinking instincts Gautam Adani gained as a diamond trader helped him build a business empire. They may well come in handy in defending it.